Converter Recycling: Recessionary Vibes, Palladium Surplus Looming

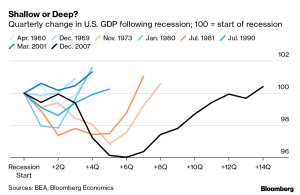

Are you feeling recessionary vibes? Some of the following signs are pointing to a US recession. A rise in interest rates and inflation. An inversion of the yield curve where the 2-year Treasury bill yielding more than the 10-year. A slowdown in consumer spending. The slowing of manufacturing activity. Unemployment is low, a counter signal, but so is workforce participation. There have been 14 U.S. recessions since the 1930s lasting an average of 14 months with a contraction in Gross Domestic Product (GDP) of 2.5% followed by 47 months of GDP expansion of 25%.

What does this mean for precious metals? The most widely followed precious metal would be gold. Gold typically does well six months before and six months after a recession, returning 28% on average, outperforming the S&P 500 by 37%. Investopedia summarizes the macroeconomic factors as follows. The price of gold is generally inversely related to the value of the U.S. dollar

because the metal is dollar denominated. All else being equal, a stronger U.S. dollar tends to keep the price of gold lower and more controlled, while a weaker U.S. dollar is likely to drive the price of gold higher through increasing demand (because more gold can be purchased when the dollar is weaker). As a result, gold is often seen as a hedge against inflation. Inflation is when prices rise, and by the same token, prices rise as the value of the dollar falls. As inflation ratchets up, so does the price of gold. The impact of inflation and the value of the dollar can be seen in the recent price action of gold. As inflation soared in 2022, the price of gold declined throughout much of the year, partly owing to the strength of the dollar against other world currencies. However, after hitting a low of less than $1,630 per ounce in September and October 2022, the price of gold began to recover, with the persistence of inflation and concerns about a recession bolstering prices throughout the fourth quarter and into 2023.

What does this mean for the platinum group metals (PGMs), platinum, palladium, and rhodium, found in scrap catalytic converters? The price of platinum and palladium has fallen in every recession except one. It is not surprising since automotive demand accounts for 40% of platinum, and 80 – 90% of palladium and rhodium. People don’t tend to purchase vehicles during times of economic downturns. Currently global vehicle sales are up 1.6% year over year, but down 5.4% over Q4 2022. Vehicle sales forecast to increase 6% to 86 M, still down over a million units a year, 15% since 2017. Right now, the US auto industry doesn’t have a supply problem, it has a demand problem. Instead of mass-producing vehicles, they are producing vehicles on demand. Auto dealers do not mind since they are selling vehicles at a premium without paying auto makers floor plan financing, further increasing their profitability.

What is the short-term and long-term outlook for each of the three metals contained in catalytic converters? Most analysts that we follow remain bullish on the three metals in the short term but warn that the recycled ounces of palladium are set to more than double from 2.5 million troy ounces to 7 million troy ounces in the next 7 years, the first surplus since Russian stock sales declined in 2013. We could see palladium at $500 – $800 a troy ounce by the 2030s. Platinum is supported in the short and long term by power curtailment in South Africa leading to a backlog of unprocessed metal and lower outturn; investor demand remaining positive; more platinum being used in China heavy duty diesel; and the use of platinum in the hydrogen economy. Palladium under pressure by heavy investor sell of this year; subdued demand; automakers showing little interest in buying at the lower prices indicating that they may have hedged too much earlier or are uncertain about the future of ICE vehicle production; price struggling to maintain $1,500 level; and future surplus. Rhodium appears to be mixed in the shortterm to positive in the long term. Short term, the glass industry has all but foregone rhodium causing investor sell off; rhodium could benefit from some palladium substitution; it remains the metal of choice in controlling NOx emissions; and it may play a small role in the hydrogen economy.

It is hard to know when and if a recession will be declared by the National Bureau of Economic Research (NBER). To be sure, we will be in one by the time it is called one. It is difficult to predict the market spikes and drops. Eight years ago, the average platinum, palladium, and rhodium prices were $1,053, $691, and $919 per troy ounce respectively. The average converter price at that time was $50 a unit. Flash forward to 2021, where the average prices for the year were $1,092, $2,397, and $18,074. The average converter price was $260 a unit. To date in 2023, the average prices are $1,007, $1,557, and $8,878. The average converter price is around $125 – $150 a unit. Prices may not be 5 times what they were in 2015; however, they are still 2-3 times what they were in 2015. It is unlikely that we will see the short-term spike in rhodium that we experienced in 2008 and 2021, thirteen years apart. As recyclers you have a couple strategies to employ. Keep selling converters into the market at the same rate that you dismantled the cars, benefitting from dollar cost averaging year over year. Process the converters you have on hand, sell all or some of the metal or opt to pool the metal and sell the individual metals at a future date. Looking backward at historical prices, and forward with future uncertainty, the current PGM markets are solid. With a reputable and trusted processor, the choice is yours.

To learn more, or to stay informed on these topics, you can subscribe to our daily e-newsletter or get Platinum Group Metal prices texted twice daily to your phone, TEXT “Daily” to

844-713-PGMs (7467). You can also call us or email us at [email protected].